The market for NFTs is expanding, becoming more intricate and increasingly lucrative. Meanwhile, the need for market-liquidizing financial products has also grown in tandem with the popularity of NFTs.

One of these tools is NFT lending, a revolutionary form of loan structure gaining traction in the NFT space. It is not surprising that demand and uptake for NFT loans are rising, given the growing appeal of NFTs.

Besides, other variables are also fueling the rise in demand. For example, the value appreciation makes them an attractive asset. Additionally, borrowers have more options as more platforms are offering NFT loans.

Analysts and researchers anticipate the demand for NFT lending to continue surging over the coming months. But first, let’s take a brief look at NFT lending.

What is NFT lending?

Investors previously had only one choice when looking for a loan: their local banks. Today, hundreds of options exist for quick loans, and the terms are every so often more manageable.

However, this conventional financing approach also has considerably lower approval rates and stricter application criteria. Loans are generally not issued as promptly as they should be.

On the other hand, NFT lending, offers crypto loans without using an intermediary, using NFT assets as collateral. It strives to provide a decentralized, open-source, and transparent platform for lending financial services.

In a nutshell, NFT lending enables borrowers to collateralize their NFTs in exchange for crypto or fiat loans.

A significant problem in the NFT market drives the demand for such financial instruments. It is the less liquid nature of the NFT market!

Moreover, you must sell your NFT entirely when you decide to do so. But people want to retain access to their NFTs, not just segments of them (like in the case of NFT fractionalization).

These issues help to explain why NFT lending has recently become a booming segment. By reducing the barrier to entry, it addresses the issue of poor liquidity in NFTs while enticing more people to engage in the NFT market.

How does NFT lending work?

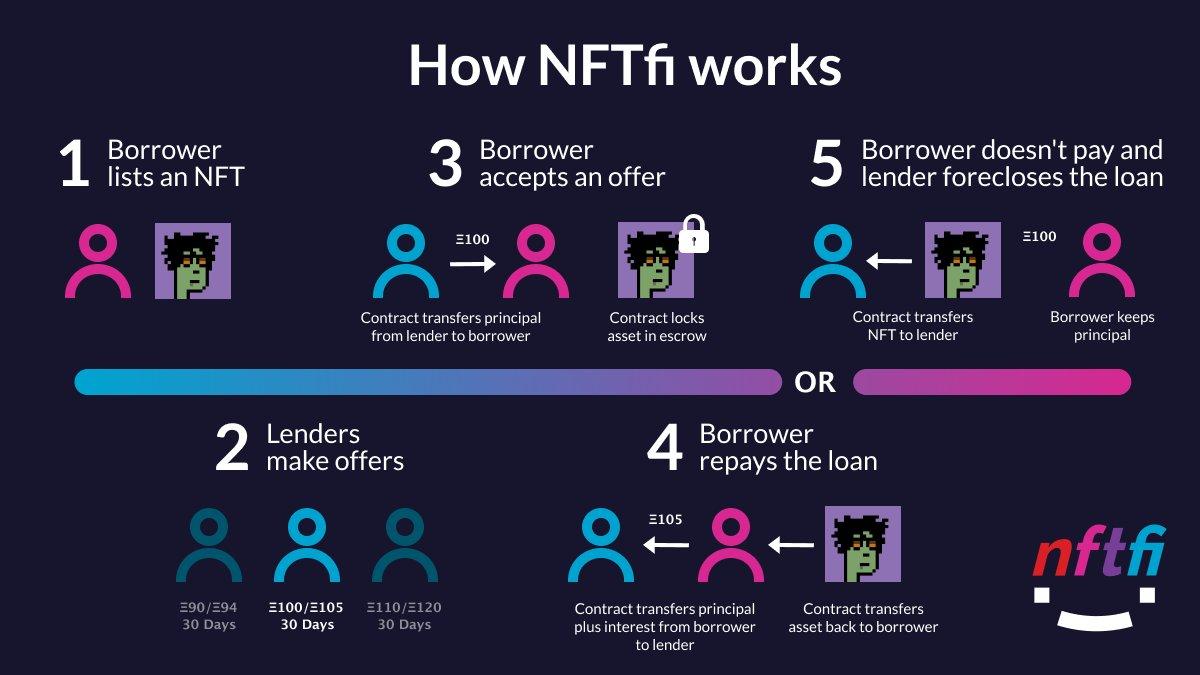

Simply put, the NFT owner gets a loan after depositing their NFT into a smart contract. The borrower must repay the loan plus interest within a given period, and the NFT’s value determines the loan sum. The lender may take possession of the NFT collateral if the borrower defaults on the debt. The borrower can reclaim the NFT collateral after repaying the debt.

Platforms for NFT lending enable NFT investors to set their own conditions and prices for borrowing digital assets. Based on the asset’s valuation, a borrower can usually obtain a loan for up to 50% of the NFT’s value at interest rates ranging from 20 to 80%.

Compared to conventional loan platforms, NFT lending mechanisms are less complicated, more transparent, and way faster. No intermediaries are involved in assessing your credit history and verifying your identity, a tiring process that takes days or weeks to decide whether to accept or refuse your application.

DeFi apps employ Smart Contracts to give users complete power over their assets. The collateral is locked in an automated smart contract.

Lenders assess the collateral’s “fair worth” by looking at previous NFT trades and the floor prices of related collections. After both parties have agreed on the conditions, the borrower moves the NFT from their wallet to an escrow system, and the protocol takes care of the rest. The NFT is forfeited if the user doesn’t pay back the debt and interest within the allotted time.

Pros and Cons of NFT Lending

Pros

- Liquidity- By loaning out assets rather than waiting for a buyer to show interest in their NFT, NFT lending can offer NFT owners a faster way to access fiat or crypto liquidity.

- Access to Capital- NFT lending enables owners to obtain immediate cash flow, which can be crucial in some situations.

- Ownership Retainment- In a financial emergency, you can use your NFTs as collateral to obtain a loan without losing ownership of your cherished digital collectibles (however, it’s crucial to ensure timely repayment of the loan).

- Portfolio Diversification- Owners of NFT disperse their investments across a variety of assets when they briefly exchange their tokens for other crypto or fiat. As long as they adequately handle loan deadlines, NFT lending could complement a sensible risk management strategy.

- Reduced Risks- NFT lending offers an opportunity for individuals to invest in NFTs without the need to purchase them upfront, thereby reducing their financial exposure to the loan term. If the value of the NFT in question decreases, the borrower may be left with an asset worth less than the initial loan agreement.

Cons

- Owners could lose NFTs perks and utilities.

- If a borrower is unable to repay a loan, they could risk losing the asset.

- Lenders may also incur losses if the NFT they accepted as collateral is overvalued.

- Smart Contract risks

- Regulatory risks

Exploring NFT Lending: A Look at Different Models and Approaches

The counterparty for users is a crucial distinguishing factor between NFT lending and borrowing models. Following this line of reasoning, we can categorize the NFT loan models around the following four models:

- Peer-to-peer NFT lending.

- Peer-to-protocol NFT lending.

- Non-fungible debt positions.

- NFT rentals.

1. Peer-to-peer NFT lending

This NFT lending mimics the traditional structure of a loan marketplace by matching lenders and debtors.

A notable example of a P2P NFT lending platform would be NFTfi. You get loan proposals from other users when you post your NFT as collateral on the site. If any agreements appeal to you, you can choose one, and the loan user’s wallet will instantly send you WETH or DAI.

The platform will immediately move your NFT into an escrow Smart Contract for the duration of the loan. When you repay the loan before the due date, NFTfi will return your NFT to your wallet. But, if you cannot repay your debt, the lender will buy your NFT at a steep markdown.

Another popular platform for peer-to-peer NFT lending is Arcade (previously known as Pawn.fi). With Arcade, users can combine numerous NFTs (for example, some few CryptoPunks) into a singular wrapped NFT that they can collateralize as a single asset.

2. Peer-to-protocol NFT lending

While peer-to-peer NFT lending offers tailored credit terms, peer-to-protocol lending facilitates borrowing straight from the protocol.

These NFT lending platforms, like the DeFi lending protocol, depend on liquidity providers depositing crypto funds into a protocol pool. Borrowers can get cash immediately after securing their NFTs as collateral and locking them up in the protocol’s digital vaults, powered by smart contracts.

A widely used platform that uses the peer-to-protocol model is BendDAO. It utilizes Chainlink oracles, which act as connectors between blockchains and data streams, to obtain information on the floor price from OpenSea, the leading NFT marketplace.

BendDAO liquidates collateralized NFTs when the collection’s floor price drops below a predetermined health factor (a native metric accounting for the NFT collateral’s market value and the borrowed sum). However, there is a 48-hour waiting time before any liquidation takes place, allowing the owner of the NFT an opportunity to save their prized NFT.

By March 2023, the protocol had about 56,711 NFTs collateralized, including 508 NFTs from the Bored Ape Yacht Club.

3. Non-fungible debt position

A non-fungible debt position (NFDP), which stands in for a specific loan agreement, is established in this approach.

The NFDP serves as a transparent log of the lending arrangement, ensuring that the conditions are not modified. It is secured and stored on a blockchain.

Moreover, users can sell NFDP on a secondary market or seamlessly transfer ownership of the NFT, giving users more flexibility in exiting a transaction or leveraging their current NFDP asset.

JPEG’d is a popular platform that offers non-fungible debt options using this NFPD. It allows users to borrow a synthetic stablecoin, $PUSd, linked 1:1 to the US dollar and collateralize blue-chip NFTs like CryptoPunks.

Borrowers who hold $PUSd can use it to provide liquidity to the protocol and earn interest or convert it to other cryptocurrencies.

JPEG’d employ Chainlink oracles to monitor the market price of its NFT collaterals, much like peer-to-pool lending systems like BendDAO.

4. Renting out NFTs

Unlike traditional lending models, NFT rentals differ as NFT perks, such as community or club membership or the opportunity to get exclusive merch. These perks are more crucial to renters than interest.

Most leasing arrangements for non-fungible tokens (NFTs) do not stipulate payback conditions, interest, or liquidation because the primary utility extracted from such NFTs is non-monetary.

Instead, a collateralized NFT is moved to a different wallet for a predetermined time in return for crypto. After the time frame, the platform returns the asset to the NFT owner. Meanwhile, the renter enjoys all the perks of the NFT in question.

reNFT is a popular platform employing this model to offer a permissionless market for prospective renters and tenants with different renting terms and conditions.

As a tenant of a leased NFT, you enjoy full access to exclusive benefits such as token-gated perks like Discord servers or giveaways usually reserved for NFT holders.

Current NFT Lending Landscape

Since the beginning of 2023, NFT lending has become a growing trend as the industry sees a revival in some key metrics.

Several robust initiatives, including BendDAO, ParaSpace, JPEG’d, NFTfi, and many others, have arisen that enable users to list their NFT as collateral and borrow another asset in return.

This trend signifies a maturing of the NFT market as industry pioneers develop more use cases for these digital assets beyond just buying and selling.

At first glimpse, lending an illiquid NFT appears risky. After all, price discovery in such a volatile market can be very unpredictable. This volatility can leave investors scrambling to replenish their collateral to avoid liquidation.

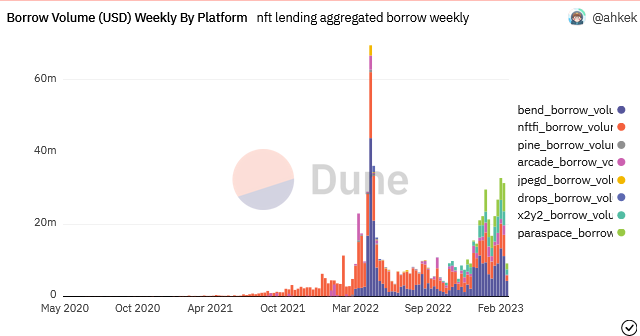

But that hasn’t stopped about $23M in lending activity across different initiatives. Dune’s data analysis of Bend, NFTfi, Pine, Arcade, JPEG’d, Drops, and X2Y2 suggests the niche has discovered a sizeable committed audience.

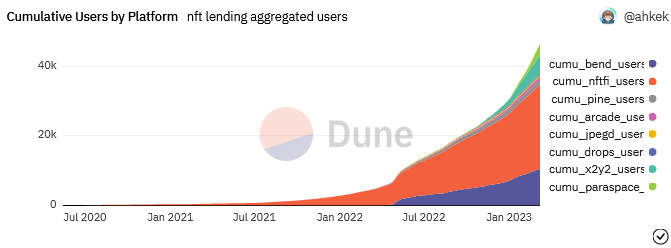

These networks’ user bases are also progressively expanding, even though the amount involved pales compared to the massive inflow of users in the DeFi gambling world.

Undeniably, the lending and borrowing platforms, with figures barely reaching 200 users per day across all projects, are becoming a noticeable trend. According to a report from The Block Research, on-chain data shows that in January, total monthly borrowing across NFT lending protocols increased to its highest since mid-2022.

Several developments, such as the recent expansion of the NFT market, the emergence of the loan protocol BendDAO, and a spike in lending activity centered on Yuga Labs’ NFTs, have fueled this trend.

According to The Block Research, BendDAO is leaving its competition in the dust, boasting an impressive market share of 43% in the lending game. Meanwhile, NFTfi trails behind with 32% of the total borrowing volume.

The success of BendDAO is attributable primarily protocol setup and its user-friendly platform, enabling users to borrow money instantly to satisfy urgent liquidity needs.

In contrast to competing protocols that use the more common peer-to-peer alternatives, BendDAO leverages a peer-to-pool model that allows users to take liquidity from the protocol by taking out loans against pools of Blue-Chip NFTs.

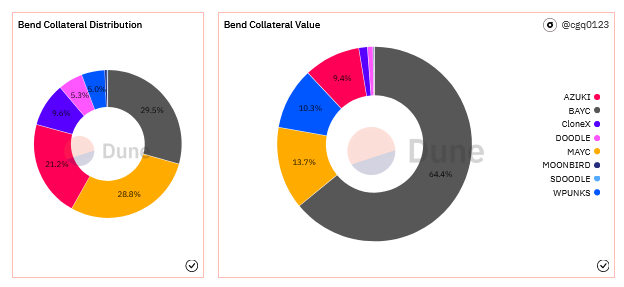

The bulk of lending and borrowing operations on BendDAO are centered around Yuga Labs’ Bored Ape Yacht Club (BAYC) and Mutant Ape Yacht Club (MAYC) collections, indicating their popularity and demand among users.

Moreover, Thomas Bialek, a researcher at The Block, claims that this has become one of the primary driving forces behind the explosion in NFT lending.

According to on-chain statistics compiled by Dune Analytics, MAYC and BAYC NFTs have accounted for the bulk of loans on BendDAO, representing 78% of the total loan value.

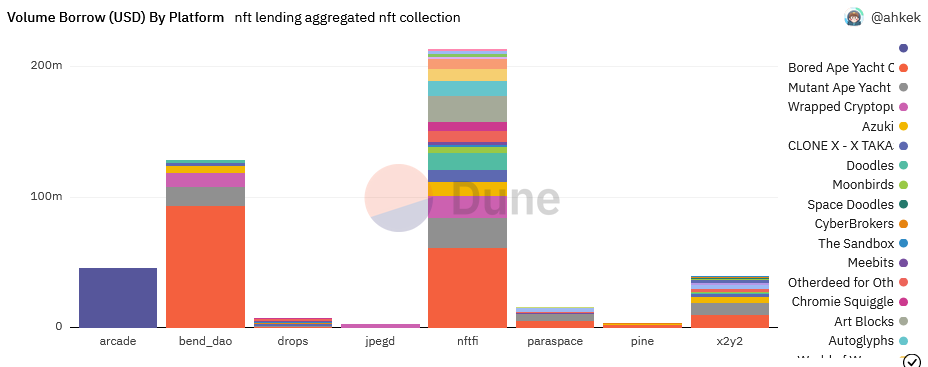

Other platforms have noticed a similar pattern. According to a report by eBit Labs, lending against Bored Apes has emerged as the frontrunner in the NFT lending space, constituting a significant portion of loans made across three prominent lending platforms: BendDAO, X2Y2, and NFTfi.

Short-dated loans for BAYC NFTs hit record highs in January, eBit labs noted, adding that a significant portion of these loans is liquidated within a day or two.

The advent of NFT lending platforms emphasizes the potential for blockchain technology to develop new financial tools that are more accessible, transparent, and efficient than conventional financial offerings.

Moreover, the fact that NFT owners can potentially earn more than the interest they have to pay on their loans shows that NFTs are not just speculative investments but also a viable asset class with real economic value.

Some DeFi powerhouses are also paying attention to this emerging niche. Last Summer, Uniswap shelled out and acquired the NFT aggregation platform Genie, dubbing its highly-anticipated NFT platform a “Google Search” for trading.

As the NFT market matures, we’ll likely see more DeFi powerhouses entering the space and offering innovative lending solutions for NFT holders.

Final Thoughts

NFT lending integrates the DeFi and NFT industries by offering much-needed liquidity to NFTs holders. These platforms provide a viable solution to traders who need instant liquidity without selling their assets or going through the tiresome screening process. It prevents buyers from cheaply dumping their NFTs on the market when they’re in a bind.

The lending market was in the spotlight in the middle of 2022, but it ran into liquidity issues when floor prices dropped. However, a revival appears to be underway at the moment.

With the continued expansion of the NFT sector, NFT lending models are likely to evolve and improve, unlocking new possibilities for asset-backed lending in the digital realm. Check out the top 4 best sites for lending.